As the dust settles in the aftermath of the financial sector collapse, and as the investment climate gradually shrugs off its state of hibernation, there is one aspect of the energy industry that has become crystal clear – the romanticism around the Renewable Energy market and the notion that it would somehow magically cure the world of all its environmental evils – has given way to the ground realities of a more prudent approach toward the development of sustainable sources for power generation. And this is not just a U.S. phenomenon. Hard lessons from Spain and Germany, takeaways from best practices in Ontario (Canada) and the allure of potentially exploding power markets in China and India, are all helping to not only shape policy decisions, but also to reset the expectations of project developers and institutional investors involved in the economics of the entire Renewable Energy sector.

The Dawn of Ground Realities

There is no denying the fact that generation from renewable sources is real and will continue to evolve as an integral part of the evolving grid infrastructure – whether as distributed generation or otherwise. The benefits – from environmental impacts to demand-side management – are many. The key question is: Who pays for it?

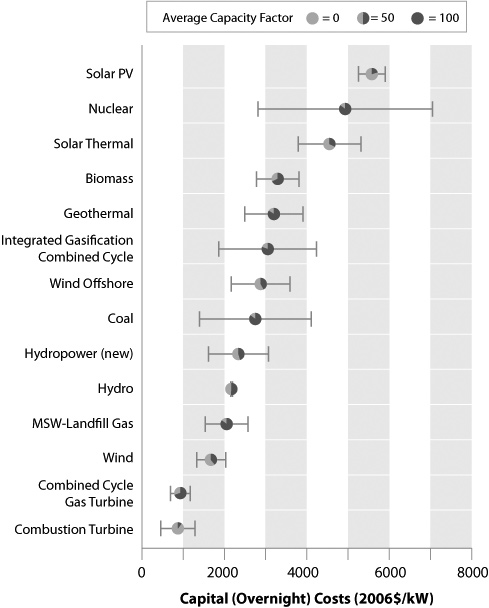

Figure 2: Plant Capacity Factors [SOURCE: NREL]

Dealing with intermittency

A simple fact has been established in every geography over the past few years that without some sort of government subsidy – whether in the form of grants, some type of feedin- tariff (FiT) structure, buy-back guarantees, or Renewable Energy Credits (RECs) – it is difficult to economically justify a solar, wind, or other alternative energy source project, apart from traditional hydro and nuclear.

Given that the sun doesn’t always shine, nor does the wind always blow when needed most, the one parameter that can make an enormous difference in competing with traditional forms of generation (e.g., coal, oil, gas, water, nuclear) is the availability of the feedstock, which impacts generation efficiency and/or plant load factor. Thus, external incentives – in the form of FiTs and RECs) – have to be brought to bear to compensate for the intermittency of the generation source. Moreover, it is imperative to improve plant capacity factors for some of the more popular forms of renewable sources, such as solar and wind.

Today, at large commercial deployments, some of the older wind projects are at about 23-27% efficiency. Newer, more efficient wind turbines have helped increase that to almost 35%. In the case of photovoltaic (PV) solar projects, the crystalline modules offer up an efficiency of as much as 17-19% from tier-1 suppliers, while some of the thin-film technologies are pushing the envelope at about 11-12%, resulting in plant capacity factors in the 20-22% range. Notably, a solar thermal array – without storage – can raise that capacity factor to an enviable 35%! A viable alternative – which is making a major resurgence – is biomass-based generation (via either combustion or gasification process) where plant capacity factors can be higher than 90%. However, the key that determines the economic viability of a biomass project is the long-term guarantee of the source and price of the feedstock.

So, what is different today? Making renewable projects investorgrade…

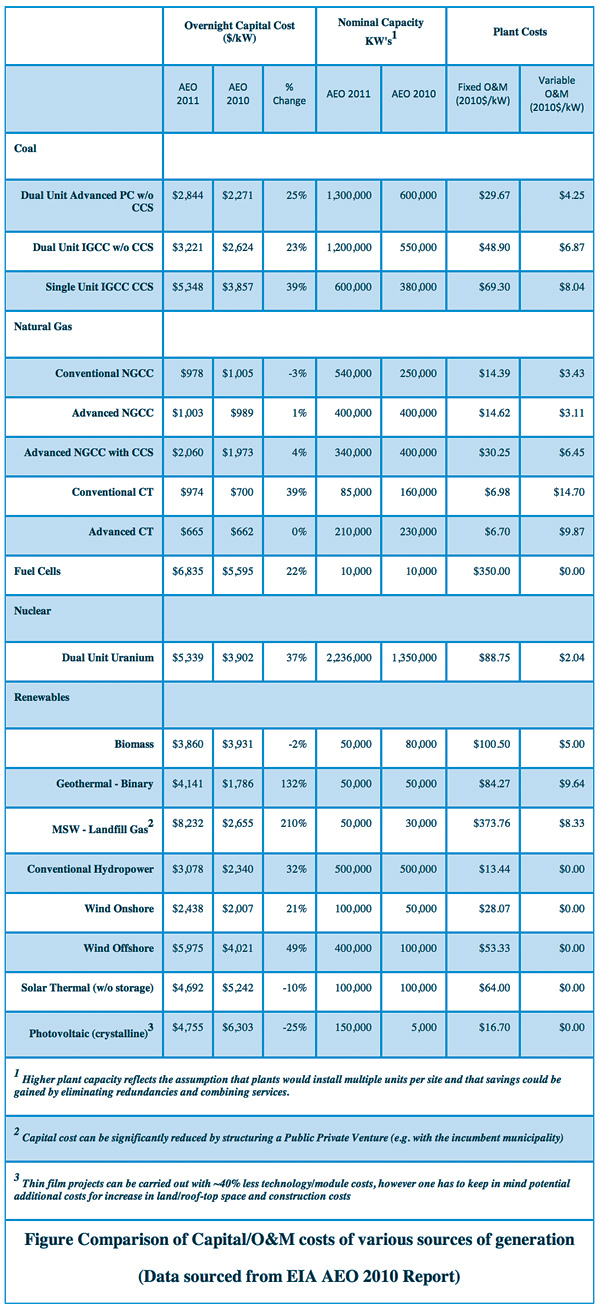

Figure 1: Comparison of Capital/O&M costs of various

sources of generation (SOURCE: EIA AEO 2010 Report)

Capital & Operational Efficiencies: To grasp what has changed one needs to first appreciate where the Cleantech sector was, as recently as eighteen months ago, globally. Did somebody say grid parity? Well, grid parity has been the utopia the alternative energy technology industry has been pushing hard. It is clear we’re not there yet, but technology has improved to a point today – either in the form of concentrated PV, or higher efficiency tilt-rotor wind turbines, or even hydrogen turbine generation (HTG) technologies – that it has started to make economic sense from two points of view: 1) An initial per MW capital cost perspective, and 2) an improving LCoE (Levelized Cost of Energy); arguably the two key factors in determining financial viability of any power project.

Thus, a project developer has to pick its battle on what form of renewable project will make sense from an investor’s perspective, taking into account not only the capital costs involved, but also how much of the regulatory hurdle a developer needs to cross, be it in terms of site control, permitting or PPA acquisition, before a project is deemed investor-ready.

Capability to Execute: Also gone are the heady days of pre-2008 when every owner of a hundred acres of land threw their hat in the ring as wind and solar developers. Today, investors and the regulators are looking for better credentials than merely land ownership. Just as it takes a village to raise a child, it takes a team of credible professionals to execute a power project. That means, a team experienced in:

Fund Raising: Without access to capital, all discussions are academic

Commercial Real Estate Management: With the increasing visibility of creating solar REITs (real estate investment trusts) for example, this is an important aspect of any renewable project development.

Power Project Development: Negotiating permits and power offtakes in the form of Power Purchase Agreements (PPAs) is more than half the battle!

Various Alternative Forms of Generation: This includes versatile, flexible strategies, such as optimization of commercially available technologies.

Engineering, Procurement & Construction (EPC): In the post development of a project this is the single most important team that can make or break any power project; and finally,

Operations & Maintenance (O&M): It is clear that both institutional (e.g., private equity and hedge funds) and corporate investors continue to believe and back credible entities – a fact that has been exemplified in the recent past with the market valuations of SunEdison’s (acquired by MEMC) and Recurrent Energy’s (acquired by SHARP Solar) project development pipeline.

Some government involvement is a good thing… up to a point!

No one likes big government and even less, a government’s involvement in a privately funded power project. This behavior is timeless… before and after any economic downturn. However, in times like this, when liquidity in the market is at a premium and when developers have scores of projects they are trying to get funded, one realizes the strategic value of a state’s support. Till most renewable projects achieve the nirvana of “grid parity” we need to face up to the fact that without some help from the government, no renewable project will see the light of day for at least the next two to three years.

Policy Measures: Germany is probably the shining example of how to foster growth of environmentally sustainable forms of generation – particularly wind and solar – and yet not bankrupt itself in the process. Although Spain became the poster child of the solar industry with an industry leading FiT model, the oversubscription of its renewable portfolio mandate also ended up adding an enormous level of stress to its already strained coffers. And the province of Ontario (Canada) is currently experimenting with a high FiT structure to bolster growth of solar energy… lessons from Spain will also help keep economic viability in check.

China is on a tear. They are trying to not only supply their own needs for renewable power but is also fast becoming the major hub for supplying technology to the rest of the world. Countries such as India – which happens to have one of the best solar, wind and biomass potential in the world and, has the government transparency to boot – has leveraged “best practices” from both Europe and North America to craft legislation. As a result, an influx of major U.S. and European players to get a piece of the pie has already started.

State subsidies: The fact is, without the DOE-sponsored ARRA grant (Section 1603) in the U.S., most developers and investors would have shied away from promoting solar, wind and biomass projects over the past eighteen months. And the extension of the DOE grant for another 12 months (through end of 2011, as of now) will help sustain that growth pipeline.

The challenge in the United States is not so much the Federal/ DOE oversight as it is the rather non-uniform fragmented approach being taken; that is, each state has its own policy.

Some form of a FiT driven market has been established in a handful of states (California and Florida have taken the lead in that regard), while states such as New Jersey and Massachusetts (the most recent entrants) are trying to foster growth of solar via the Solar Renewable Energy Credit (SREC) market. Even with these state sponsored incentives, however, most private investors are wary of the sustainability of such measures. In order for the path to clear, there needs to be a line of sight to long-term SREC pricing structures to determine serviceability of a project’s debt and equity needs.

In this author’s opinion, such market-driven incentives should be a collaborative effort – the government defining the basic overarching policy that facilitates project development (versus growth-stifling rules and restrictions), while the market’s supply and demand mechanism uses the policy framework to define rate and pricing structures.

Where it’s still hurting: Although not necessarily at a grinding halt, the frenzy of wind development over the past five years has taken a hit due specific challenges that can be avoided with more support from regulators and collaboration with the investment community. An average cycle-time to close permitting and interconnection contracts now approaches almost two years in some cases… and that’s for onshore projects! This kind of drawn out project schedule can cause the entire economic model for the project to turn on its head by the time it reaches the construction phase.

Moreover, it can take a grid-tied solar project (i.e., one that will be connected to the Transmission system) about nine months just to get interconnection clearance from an ISO… when an entire solar project can be constructed within six months! These timelines – which are uncertain at best – pose enormous strain on funds that are required by a developer to just “stay the course”… and most investors are not interested in funding small developers.

Koustuv Ghoshal is Managing Partner at Inspirra Energy, an independent investment banking and industry advisory firm focused on the mid-market renewable project development and energy efficiency sectors globally. Each of its principals has deep industry experience in energy industry market research, power project development, and project funding advisory. Koustuv can be reached by phone at +1-469-361-2120 or via email to kghoshal@inspirra.com.