In August of 2007, the National Energy Technology Laboratory (NETL) released its ‘Modern Grid Benefits’ report for the U.S. Department of Energy’s Office of Electricity Delivery and Energy Reliability as part of the NETL Modern Grid Initiative, Powering our 21st-Century Economy. It is a useful look at the seven principal characteristics that NETL identified eight years ago to launch the grid transformation, the progress made, and what the grid of the future looks like today.

Given the current focus on grid modernization and the grid of the future, have we made progress? We asked Gary Rackliffe, vice president of Smart Grids for ABB in North America, to answer that question and share his views on where he thinks the grid and the power industry is headed over the next decade.

EET&D : What did NETL define as the principal characteristics needed to meet the demands of the 21st century?

Rackliffe : In 2007 NETL identified seven essential characteristics needed for the grid of the 21st century. These characteristics define a grid that can 1) be self-healing, 2) engage the consumer, 3) resist attack, 4) provide power quality, 5) accommodate all generation and storage options, 6) enable markets, and 7) optimize assets and operate efficiently.

EET&D : Do these grid characteristics create benefits?

Rackliffe : Yes. NETL identified significant benefits related to eliminating cascading outages, increasing national security, reducing reliance on imported fuel, reducing energy losses, more efficient generation, better power quality, lower environmental impact, improved U.S. competitiveness, and new customer benefits. Smart grid benefit to cost ratios previously estimated by the Electric Power Research Institute (EPRI) range from 2.8 to 6.0 and market analysts continue to be positive for technologies that improve reliability and resiliency or that improve generation capacity utilization by reducing peak demand. Volt/Var optimization and demand response are examples of technologies that can reduce peak demand. The DOE also identified significant benefits from the Smart Grid Investment Grants (SGIGs) and Demonstration Projects.

More recently in February, as part of the New York State Reforming the Energy Vision proceedings, the Order Adopting Regulatory Policy Framework and Implementation Plan stated that “if, for example, the 100 hours of greatest peak demand were flattened, long-term avoided capacity and energy savings would range between $1.2 billion and $1.7 billion per year” for the state.

EET&D : What has changed on the grid?

Rackliffe : There have been several significant changes to the grid. Events such as Superstorm Sandy, the physical attack on PG&E’s Metcalf substation in California, the availability of natural gas, the impact of energy conservation and the economy on load growth, and the drop in the cost of solar PV panels have changed the landscape. Utilities now need to address physical security threats as well as cybersecurity threats.

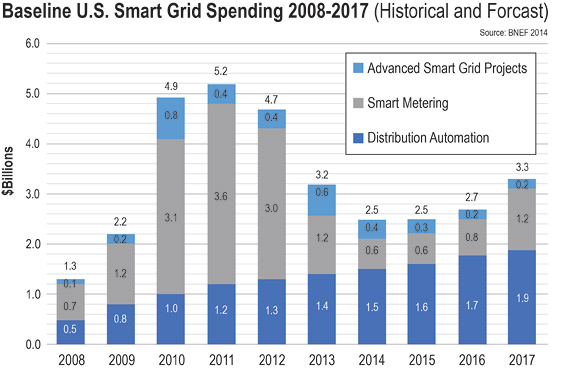

The DOE SGIGs resulted in a major investment spike in advanced metering infrastructure (AMI). These meter systems provide utility operational savings, but they also improve customer services and engagement, provide outage notification and restoration verification for storm response, and provide the foundation for new demand response initiatives. The communications infrastructure for AMI data backhaul can also support communications to distribution automation devices between the substations and meters. The SGIGs also contributed to the sustained investment growth in distribution automation technologies.

Aging infrastructure has aged an additional eight years since that 2007 NETL report. The grid assets installed as part of the transmission investment bubble in the 1970s are now 40 years old and utilities are operating assets that are 50 to 60 years old. Older assets can continue to perform, but utilities are concerned about the potential impacts to reliability and the costs to maintain and replace these aging assets. At the same time, the retirements from an aging workforce are depleting the technical resources.

Costly weather-related events increased significantly in the past decade. DOE’s Quadrennial Review released this year shows that there were 11 events causing at least a billion dollars in damage in 2008 and 2012 and the number reached 16 in 2011, new highs for these weather-related disasters. Superstorm Sandy was a wake-up call for the industry. This storm in particular highlighted how critical situational awareness is and triggered investments in grid modernization such as advanced distribution management systems (ADMS) and distribution automation, storm hardening such as elevation of substations, and grid resiliency such as microgrids.

The generation mix in the US is changing. Coal generation has decreased from generating approximately half of our electricity to about a third of the production and natural gas generation has filled the gap. The increased supply of domestic natural gas at significantly lower prices and lower emissions have contributed to this change. Wind and solar PV generation continue to grow to meet renewable portfolio standards, but they currently represent a small share of the US electricity production, even with the significant drop in the price of solar panels. The variable nature of wind and solar do stress the transmission and distribution systems respectively and have the potential to erode the efficient utilization of centralized generation under high-penetration scenarios.

Load grow has been flat. A steady growth in load has historically helped utilities, but economic growth has been decoupled from growth in electricity consumption as the economy rebuilds following the 2008 recession. As the economy has recovered, electricity consumption growth has been flat. A likely factor is the cumulative impact of energy conservation and efficiency investments.

Energy storage is now another strategic tool that utilities can use for operational effectiveness with recent trends focusing on commercialization, standardization, and pre-engineered solutions. Energy storage systems are providing ancillary services such as frequency regulation, power quality, spinning reserves, and ramp rate control and capacity firming for renewable generation. Peak shaving and load leveling are additional applications. Utilities are recognizing the strategic value of energy storage.

Finally, distributed energy resources and microgrids are emerging as key elements of the grid of the future. Demand response aggregators, third-party owned solar PV installations, and customer microgrids are part of the grid landscape and potentially threaten current utility business models.

EET&D : As we look at the grid of future, what is the focus of utilities?

Rackliffe : I would highlight distribution grid management, transmission technologies, utility analytics, and distributed energy resources. For example, reliability and grid resiliency investments have enabled utilities to reduce customer outage minutes. Advanced distribution management systems are integrating distribution SCADA, outage management, automated switching applications, mobile work force management, and business intelligence to drive improved outage life cycle management. Improved situation awareness to provide accurate assessments of storm damage and restoration time estimates are enabling stakeholder communications.

Situational awareness at the transmission level provides visualization of power oscillations, voltage stability, and improved data for state estimation. Other transmission technologies include digital substations; HVDC for grid support, regional interconnections, and connecting wind generation to load centers; and FACTS to add capacity and resiliency to the transmission grid.

EET&D : So what are the roadblocks holding us back?

Rackliffe : Two items: policy and education. Under policy, utilities are concerned about how DERs will change the existing business model and how the industry would transition. There are technology issues, but the policy alignment, largely at the individual state level, will set the pace of how the industry transitions. Some policy developments to watch:

- DOE ‘Future of the Grid’ project in collaboration with the GridWise Alliance which will establish clear and comprehensive guiding principles, along with a unifying architecture, and create a framework for guiding investments to transition from today’s grid to the future grid.

- US Court of Appeals in DC vacated FERC Order 745 and ruled against FERC’s role in demand response. The Supreme Court is scheduled to rule on the Obama Administration’s appeal later this year.

- EPA 111d Clean Power Plan establishes state emission targets that will impact generation resources. The plan will be challenged but is a part of the Obama Administration’s current agenda.

- Renewable portfolio standards, wind production tax credit, and solar PV investment tax credits will impact renewable energy investments.

- New York State’s ‘Reforming the Energy Vision’ process is moving forward to address market design and platform architecture.

- California utilities have filed Distribution Resource Plans and are procuring 1.3 GW of energy storage as required by the commission. California is also updating the Rule 21 interconnection standard.

Second, regarding education, customers must be engaged. This grid transformation and integration of DERs will require customer engagement and public support for policy change to transition to the grid of the future. To achieve the grid operational effectiveness and the economic competitive advantages that were defined by NETL and now incorporated into the current grid of the future initiatives will require consumer education.

EET&D : We can’t thank you enough Gary for finding time for us to discuss the grid of the future. With the importance of the smart grid growing exponentially, your words and thoughts couldn’t be more timely.

About the Author

Gary Rackliffe is vice president for Smart Grids for ABB Inc., leading ABB’s smart grid and distribution automation initiatives in North America and managing the ABB Smart Grid Center of Excellence in Raleigh, North Carolina. Gary has worked for ABB for more than 25 years. He is past chair of NEMA’s Smart Grid Council and member of the DistribuTECH Advisory Committee, US Department of Commerce Renewable Energy and Energy Efficiency Advisory Committee, and IEC Smart Energy Systems Committee. He serves on the Board of Directors for the Research Triangle (N.C.) Cleantech Cluster and for the GridWise Alliance. Gary holds BS and ME degrees in Power Engineering from Rensselaer Polytechnic Institute and a MBA from Carnegie Mellon University. He is based in Raleigh. Gary may be reached at: Gary.Rackliffe@us.abb.com.

Gary Rackliffe is vice president for Smart Grids for ABB Inc., leading ABB’s smart grid and distribution automation initiatives in North America and managing the ABB Smart Grid Center of Excellence in Raleigh, North Carolina. Gary has worked for ABB for more than 25 years. He is past chair of NEMA’s Smart Grid Council and member of the DistribuTECH Advisory Committee, US Department of Commerce Renewable Energy and Energy Efficiency Advisory Committee, and IEC Smart Energy Systems Committee. He serves on the Board of Directors for the Research Triangle (N.C.) Cleantech Cluster and for the GridWise Alliance. Gary holds BS and ME degrees in Power Engineering from Rensselaer Polytechnic Institute and a MBA from Carnegie Mellon University. He is based in Raleigh. Gary may be reached at: Gary.Rackliffe@us.abb.com.

Gary is scheduled to speak at the upcoming Smart Grid Canada 2015 / Smart Grid Road Show in Toronto on October 6 on the topic of microgrids and grid resiliency.