“Utilities are facing a crisis of rebirth.” That’s futurist Alvin Toffler speaking in an interview he gave last spring.

Toffler was talking about the revolutionary change he sees taking place between energy producers and sellers on the one hand and customers on the other.

In the 20th Century, he points out, the producer/consumer relationship was based on producers’ power to develop and offer new products. Consumer power was largely confined to accepting products or rejecting them. Producers’ mindset revolved around, “if we build it, they will come.” When they sought customer feedback, it was primarily to discover factors that would make customers more likely to accept, less likely to reject the product.

In the 21st Century, Toffler foresees a transition to a different type of relationship between energy producer and customer. He envisions the customer as an active participant in the development of the products that appear in the marketplace. He sees marketplace relationships becoming more complex and interdependent. He envisions a relationship in which both parties are sellers and both are buyers.

Far-fetched? Probably not.

C&Is in the Forefront

Look at commercial and industrial customers (C&Is). Yesterday, only the largest used their size and economic influence in the community to essentially write their own tickets when it came to utility services.

In the Nineties, smaller C&Is anticipated gaining some of these benefits for themselves through deregulation. But the failure of early programs—some to achieve affordable energy, others to achieve competition at all—has led to indefinite delays in states’ and provinces’ taking the next deregulatory steps. At the same time, these smaller C&Is are suffering from economic slow-downs stock-price declines that have them increasingly focused on cost cutting.

As a result, an increasing number of smaller C&Is are exchanging information and using it to work with utilities to develop new service models. Consolidated bills that permit franchisers to cut down on paperwork. Convergent bills that mesh multiple services. Bills in multiple versions sent to multiple site managers and compared at headquarters to see who’s minimizing energy costs - and who isn’t.

Smaller C&Is are also seeing advantages in tailored contracts that gear utility rates to their usage patterns and economic conditions. Increasingly, they’re proposing specific ways they and their utilities can produce under a regulated scenario the options once thought achievable only through deregulation: Access to the wholesale generation market. Device management. Supply prices and delivery mechanisms that supplement rather than dominate their use of onsite generation.

That’s not yesterday’s utility market. Today, C&Is expect to work with their utility. They expect utilities to help them achieve energy supplies and prices that support corporate competitiveness in their own tough domestic and global markets.

What About Consumers?

On first glance, residential consumers seem unlikely to adopt the C&Is’ stance—at least in the immediate future. The popular resistance to North American deregulation has fueled a belief that few consumers want power and that most will reject it when it is thrust upon them.

But wait. The “power” placed in consumer hands during the initial stages of North American deregulation was defined by regulators and large C&Is. In many states, consumers had change thrust upon them. Their "power" seemed limited to spending five or ten hours trying to understand competitive intricacies. Their reward was saving $20 or $30 a year on their electric bills.

Some consumers were further short-changed. When meaningful competition evaporated in states like Pennsylvania and New Jersey, consumers found their accounts back with the original utility. In Georgia, consumers’ time investments skyrocketed as they were forced to track down missing and inaccurate bills. And that’s not even mentioning California.

In short, many consumers have failed to receive what they believe to be an appropriate return on their time investment in competitive markets. As a consequence, their interest in exercising power in the immediate future is probably low.

New Awareness Through Information Exchange

But it may not remain low.

There is a flip side to the consumer experience with most state and provincial electricity-choice programs. It has enlarged the agendas of utility consumer groups once focused solely on rates. Broader consumer-advocacy groups have entered the fray. They are exchanging information across state, provincial, and national boundaries.

Over the next few years, consumers are likely to become aware that, with or without deregulation, a growing number of utilities offer:

Judging from the experience in other deregulating industries, information exchange can lead to new consumer demands. Utilities that fail to offer new services may soon confront consumers asking, “Why not?” Furthermore, utilities that fail to offer these services could find that customers perceive them as poorly managed or not progressive.

Speed of Evolution

Clearly, the customer revolution is coming. The question is: how quickly?

C&Is are already on the move. And many utilities are responding. The 2003 Chartwell Report on Key Accounts Service sees most energy providers—especially electric utilities—with some sort of program to handle their largest customers. In fact, about half of all utilities report a dedicated key accounts program.

But is a “we care” attitude really enough? Many utilities appear to think so. When Chartwell asked about specific services, programs appeared less than responsive. A remarkable 47 percent of those surveyed said they had no plans to offer C&Is time-of-use billing. Fifty-three percent were not considering choices in billing date. Thirty-one percent failed to see electronic data interchange (EDI) on their horizons.

Service expansion for consumers is also uneven. A second Chartwell report, the Guide to Bill Presentment and Payment 2003, shows considerable movement on some fronts. More than three-quarters of all utilities, for instance, accept credit-card payments and bank debits. On the other hand, only half offer electronic bill presentment and payment (EBPP). And only 35 percent permit consumers to choose billing dates.

What about the future? Currently, Chartwell reports, 22 percent of utilities offer email bill presentment. Another 15 percent are planning to add it, and an additional 18 percent are considering the move. That’s a rapid growth rate. But it still leaves 45 percent of utilities in which email billing is not even on the radar screen.

Is utility service evolution fast enough? Or will the customer revolutionaries be at the gate before planning begins?

IT Implications

The uneven pace of response to the customer revolution results in part from the inflexibility of the customer information systems (CIS) still in place at most utilities. Designed for the singleservice, commodity emphasis of the Eighties (or the Seventies, or even the Sixties!), these legacy CIS systems cannot accommodate new service offerings without significant change.

Utilities are hamstrung if they approach CIS replacement from the point of view of a single new service. Cost-benefit justification for system replacement does not emerge. Given that even the best established EPBB programs, for instance, report only about 4-5 percent customer usage, only the foolhardy would suggest that a utility spend $2 million to offer Internet bill payment to its 70,000 customers.

The analysis is different, however, when a utility places system-replacement costs against the dozens of potential new services available through the same system change.

Change becomes even more compelling when additional new-system advantages are included: faster rate changes; environmentally sensitive options for customers like “green electricity”; reduced training time; less vulnerability to the retirement of those few programmers who understand the intricacies of the current system. And change becomes an imperative as utilities begin to consider the home-sized fuel cell. Once customers become generators, their demands to participate in the overall design and direction of electricity infrastructure are likely to swell rapidly.

Customers Are Marching

There’s little doubt that utility customers of all sizes are starting to want more—and will increasingly vocalize their desires in the future. A new report from the Consumer Energy Council of America demands residential choices like advanced metering, alternative pricing methodologies, and products that help consumers make environmentally sound choices. Phrases like “virtual choice” and “virtual competition”—an approach to energy distribution that demands utilities offer consumers options—are becoming commonplace among policymakers.

But the customer revolution does not have to be threatening. Revolutionaries man the barricades only when demands are met with resistance. Why not join the revolution instead? By making plans and infrastructure changes now, utilities will be able to welcome a generation of highdemand consumers and turn the customer revolution into a springboard for improved customer service and satisfaction.

About the Author

David Mulit is general manager for the Americas at customer-information-solution vendor SPL WorldGroup. He previously worked for a large gas and electric utility for sixteen years. You can see more of the interview with Alvin Toffler on the future of utilities at http://www.splwg.com/main/news/articles/ April2003_SPLprofile.pdf

Toffler was talking about the revolutionary change he sees taking place between energy producers and sellers on the one hand and customers on the other.

In the 20th Century, he points out, the producer/consumer relationship was based on producers’ power to develop and offer new products. Consumer power was largely confined to accepting products or rejecting them. Producers’ mindset revolved around, “if we build it, they will come.” When they sought customer feedback, it was primarily to discover factors that would make customers more likely to accept, less likely to reject the product.

In the 21st Century, Toffler foresees a transition to a different type of relationship between energy producer and customer. He envisions the customer as an active participant in the development of the products that appear in the marketplace. He sees marketplace relationships becoming more complex and interdependent. He envisions a relationship in which both parties are sellers and both are buyers.

Far-fetched? Probably not.

C&Is in the Forefront

Look at commercial and industrial customers (C&Is). Yesterday, only the largest used their size and economic influence in the community to essentially write their own tickets when it came to utility services.

In the Nineties, smaller C&Is anticipated gaining some of these benefits for themselves through deregulation. But the failure of early programs—some to achieve affordable energy, others to achieve competition at all—has led to indefinite delays in states’ and provinces’ taking the next deregulatory steps. At the same time, these smaller C&Is are suffering from economic slow-downs stock-price declines that have them increasingly focused on cost cutting.

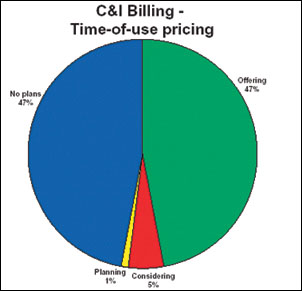

The 2003 Chartwell Report on Key Accounts Service reports that only about half of all utilities offer timeof- use billing to commercial and industrial customers. (Graph used with the permission of Chartwell, Inc.,

As a result, an increasing number of smaller C&Is are exchanging information and using it to work with utilities to develop new service models. Consolidated bills that permit franchisers to cut down on paperwork. Convergent bills that mesh multiple services. Bills in multiple versions sent to multiple site managers and compared at headquarters to see who’s minimizing energy costs - and who isn’t.

Smaller C&Is are also seeing advantages in tailored contracts that gear utility rates to their usage patterns and economic conditions. Increasingly, they’re proposing specific ways they and their utilities can produce under a regulated scenario the options once thought achievable only through deregulation: Access to the wholesale generation market. Device management. Supply prices and delivery mechanisms that supplement rather than dominate their use of onsite generation.

That’s not yesterday’s utility market. Today, C&Is expect to work with their utility. They expect utilities to help them achieve energy supplies and prices that support corporate competitiveness in their own tough domestic and global markets.

What About Consumers?

On first glance, residential consumers seem unlikely to adopt the C&Is’ stance—at least in the immediate future. The popular resistance to North American deregulation has fueled a belief that few consumers want power and that most will reject it when it is thrust upon them.

But wait. The “power” placed in consumer hands during the initial stages of North American deregulation was defined by regulators and large C&Is. In many states, consumers had change thrust upon them. Their "power" seemed limited to spending five or ten hours trying to understand competitive intricacies. Their reward was saving $20 or $30 a year on their electric bills.

Some consumers were further short-changed. When meaningful competition evaporated in states like Pennsylvania and New Jersey, consumers found their accounts back with the original utility. In Georgia, consumers’ time investments skyrocketed as they were forced to track down missing and inaccurate bills. And that’s not even mentioning California.

In short, many consumers have failed to receive what they believe to be an appropriate return on their time investment in competitive markets. As a consequence, their interest in exercising power in the immediate future is probably low.

New Awareness Through Information Exchange

But it may not remain low.

There is a flip side to the consumer experience with most state and provincial electricity-choice programs. It has enlarged the agendas of utility consumer groups once focused solely on rates. Broader consumer-advocacy groups have entered the fray. They are exchanging information across state, provincial, and national boundaries.

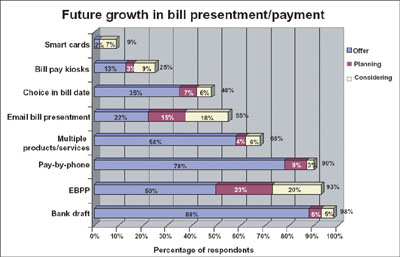

A number of utilities offer multiple billing-related services, according to Chartwell’s Guide to Bill Presentment and Payment 2003.

(Graph used with the permission of Chartwell, Inc.,

Over the next few years, consumers are likely to become aware that, with or without deregulation, a growing number of utilities offer:

- Billing flexibility. Some utilities permit consumers to choose the date on which their billing cycle closes. That’s an option particularly popular with senior citizens, who can match billing dates to receipt of pension checks. Other utilities provide duplicate bills. That provides another senior-citizen benefit: the out-of-state children of elderly parents can more easily assist will bill payment.

- Convergent billing. This permits households to pay for multiple services with one check.

- Bill payment options. On-line, credit card, automatic debit are popular Kiosk use is on the rise.

- Loyalty programs that offer premiums (like frequent- flyer miles) and rebates on utility bills.

- "Green electricity" programs. Some permit consumers to purchase varying amounts of electricity from renewables and to change that amount frequently.

- Surge protection insurance.

- Guarantees against the consequences of interruptions in electricity or gas service.

Judging from the experience in other deregulating industries, information exchange can lead to new consumer demands. Utilities that fail to offer new services may soon confront consumers asking, “Why not?” Furthermore, utilities that fail to offer these services could find that customers perceive them as poorly managed or not progressive.

Speed of Evolution

Clearly, the customer revolution is coming. The question is: how quickly?

C&Is are already on the move. And many utilities are responding. The 2003 Chartwell Report on Key Accounts Service sees most energy providers—especially electric utilities—with some sort of program to handle their largest customers. In fact, about half of all utilities report a dedicated key accounts program.

But is a “we care” attitude really enough? Many utilities appear to think so. When Chartwell asked about specific services, programs appeared less than responsive. A remarkable 47 percent of those surveyed said they had no plans to offer C&Is time-of-use billing. Fifty-three percent were not considering choices in billing date. Thirty-one percent failed to see electronic data interchange (EDI) on their horizons.

Service expansion for consumers is also uneven. A second Chartwell report, the Guide to Bill Presentment and Payment 2003, shows considerable movement on some fronts. More than three-quarters of all utilities, for instance, accept credit-card payments and bank debits. On the other hand, only half offer electronic bill presentment and payment (EBPP). And only 35 percent permit consumers to choose billing dates.

What about the future? Currently, Chartwell reports, 22 percent of utilities offer email bill presentment. Another 15 percent are planning to add it, and an additional 18 percent are considering the move. That’s a rapid growth rate. But it still leaves 45 percent of utilities in which email billing is not even on the radar screen.

Is utility service evolution fast enough? Or will the customer revolutionaries be at the gate before planning begins?

IT Implications

The uneven pace of response to the customer revolution results in part from the inflexibility of the customer information systems (CIS) still in place at most utilities. Designed for the singleservice, commodity emphasis of the Eighties (or the Seventies, or even the Sixties!), these legacy CIS systems cannot accommodate new service offerings without significant change.

Utilities are hamstrung if they approach CIS replacement from the point of view of a single new service. Cost-benefit justification for system replacement does not emerge. Given that even the best established EPBB programs, for instance, report only about 4-5 percent customer usage, only the foolhardy would suggest that a utility spend $2 million to offer Internet bill payment to its 70,000 customers.

The analysis is different, however, when a utility places system-replacement costs against the dozens of potential new services available through the same system change.

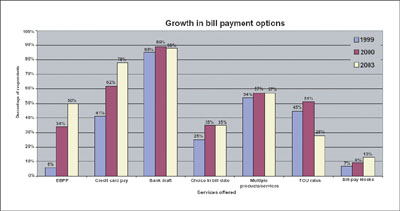

More services are on the way. But many utilities are not yet considering billing options that have become routine in other markets.

(Graph from Chartwell’s Guide to Bill Presentment and Payment 2003; used with permission.)

Change becomes even more compelling when additional new-system advantages are included: faster rate changes; environmentally sensitive options for customers like “green electricity”; reduced training time; less vulnerability to the retirement of those few programmers who understand the intricacies of the current system. And change becomes an imperative as utilities begin to consider the home-sized fuel cell. Once customers become generators, their demands to participate in the overall design and direction of electricity infrastructure are likely to swell rapidly.

Customers Are Marching

There’s little doubt that utility customers of all sizes are starting to want more—and will increasingly vocalize their desires in the future. A new report from the Consumer Energy Council of America demands residential choices like advanced metering, alternative pricing methodologies, and products that help consumers make environmentally sound choices. Phrases like “virtual choice” and “virtual competition”—an approach to energy distribution that demands utilities offer consumers options—are becoming commonplace among policymakers.

But the customer revolution does not have to be threatening. Revolutionaries man the barricades only when demands are met with resistance. Why not join the revolution instead? By making plans and infrastructure changes now, utilities will be able to welcome a generation of highdemand consumers and turn the customer revolution into a springboard for improved customer service and satisfaction.

About the Author

David Mulit is general manager for the Americas at customer-information-solution vendor SPL WorldGroup. He previously worked for a large gas and electric utility for sixteen years. You can see more of the interview with Alvin Toffler on the future of utilities at http://www.splwg.com/main/news/articles/ April2003_SPLprofile.pdf