Systems are only as good as their uptime. No one understands this more than utility managers, who told Black & Veatch in the company’s 2018 Strategic Directions: Electric Industry Report that the long-time challenges of reliability, security and infrastructure are just as important today as they have been in years past.

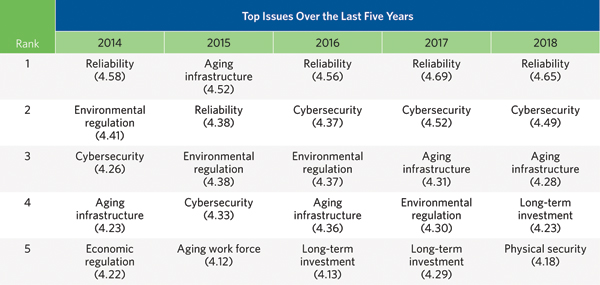

When asked what critical issues haunt the electric sector today, survey respondents pointed to familiar challenges – grid reliability, cybersecurity and aging infrastructure, long-term investment and physical security as important or very important issues (Figure 1).

These responses have consistently ranked among the most pressing concerns for the power sector over the past five years. Reliability – the ability to provide consistent service to consumers – sits at the heart of these issues because it mandates that operations continue unabated despite cyber attacks, grid-battering storms, power-quality issues or simple failure of decades-old equipment that’s reached the end of its useful life.

Figure 1. Please rate the importance of each of the following issues to the electric industry using a 5-point scale, where a rating of 5 means “Very Important” and a rating of 1 means “Not Important at All.” (Please select one choice per row)

Source: Black & Veatch

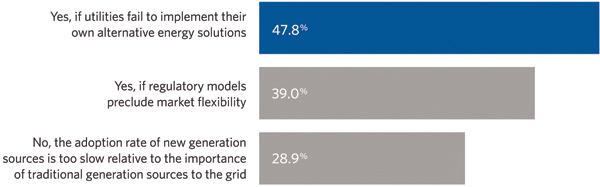

Figure 2. Do you perceive this “utility death spiral” as a real, potential outcome? (Select all that apply).

Source: Black & Veatch

What complicates the reliability challenge is the financial uncertainty utilities face in the so-called “utility death spiral.” Utilities and the regulatory bodies that oversee them must find a way to keep power providers viable, or the industry may have a hard time meeting reliability goals and, perhaps, even surviving.

Death Spiral and Taxes

By definition, the death spiral is that ugly Catch-22 that occurs when more and more customers switch to self-generation and drop from the traditional grid, except for the need of a provider of last resort. That makes power more expensive for remaining customers unless fixed infrastructure costs can be equitably recovered.If utilities raise rates for remaining customers, the added costs could make self-generation even more attractive, and the spiral widens.

Such a situation would occur if utilities fail to implement their own alternative energy solutions or if regulatory models preclude market flexibility, survey respondents agreed.

The utility death spiral wasn’t on the above issues list in the Strategic Directions survey – rather, it warranted its own question. According to survey results, most utility survey respondents see the death spiral as a real, potential outcome (Figure 2).

Customers are certainly jumping into the power supply game. The business community is making a strong commitment to alternative energy. Under the RE100 banner, more than 120 multinational giants — including Apple, Walmart, Bank of America, General Motors, Starbucks, eBay, Kellogg’s, Hewlett-Packard and more — have announced a goal of 100-percent renewable energy. In April, Apple announced that all of its global data centers, retail stores and offices in 43 countries now are 100-percent powered by renewable electricity, either from solar or wind power.

Many companies are generating their own energy through rooftop solar and buying renewable-based power from offsite grid-connected generators. In a recent surveyof RE100 participants, companies said that in addition to the environmental benefits, the business case for switching to renewable energy is becoming stronger. Sustainable energy is now more than environmental policy; it is a competitive advantage.

This should be particularly alarming to utilities because C&I accounts make up two-thirds of U.S. electricity use, according to data from the Energy Information Administration. Along with declining sales, utilities will need to accommodate behind-the-meter renewables.This will take a new game plan.

What’s in Storage?

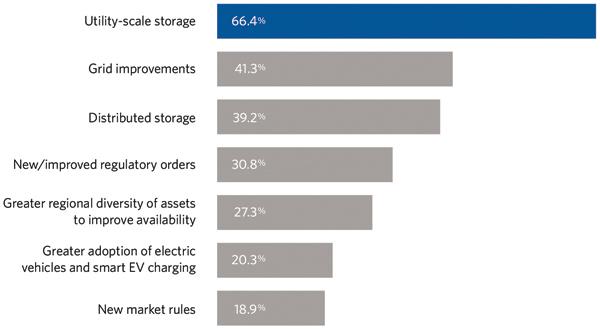

Findings from the Strategic Directions: Electric Report survey reveal what energy professionals are thinking as they plan and build their renewables projects. When asked to choose the best options for renewable integration, utility-scale energy storage was the preferred choice at 66 percent, with grid improvements coming in a distant second at 41 percent (Figure 3).

The dropping cost of storage technology is good news for utilities because high prices long have been a challenge to integration efforts. Today’s lower costs are enabling much more competitive offerings, as seen recently in Colorado. There, Xcel Energy received bids from energy developers to supply solar and wind-generated electricity — with battery storage included — at a lower cost than conventional generation. While Colorado’s supportive regulatory environment helped make this a reality, the takeaway from this development shows that renewable energy at utility scale can be price-competitive with fossil fuels and even cost less.

Along with battery energy storage systems, there are other ways to address intermittency without investing in new equipment or infrastructure. Survey respondents were asked what system improvements they recommend.

A variety of tools are available to help utilities deal with the variability of renewables, including demand management, storage management, real-timemonitoring and rapid cutover solutions to meet a sudden dropin output.

For example, demand response no longer means that businesses or residential customers will have their power interrupted for an hour or more during peak energy demand periods. Demand response management systems now use machine learning to facilitate aggregationof load shedding that lets utilities power down just a few devices at a site for brief periods, leaving the customers participating in these programs nearly undisturbedby load shedding events.

More accurate forecasting of wind and solar outputis another lever, as it is changing the way power producers are incentivized or potentially penalized for over- or under-generation.

The most popular choice was quick response resources, selected by 56 percent of survey participants, followed closely by load control devices (51 percent) and advanced system control devices (48 percent). Utilities typically use a combination of the resources listed. While these are admittedly partial measures, they can help grid operators respond to output fluctuations with minimal investment.

Figure 3. Where do you see the best options for utility-scale renewable integration? (Select up to three choices)

Source: Black & Veatch

Finding the Funding

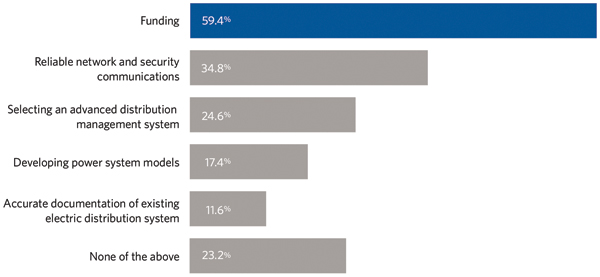

There’s no doubt about it: Integrating renewables and DG will require new funding mechanisms. Knowing the proliferation of DER will continue with increasing speed, utilities report that finding the money is the biggest hurdle they face to implementing the distribution system of the future they’ll need to make widespread distributed generation viable.

On the regulatory front, states are making momentous decisions that will significantly impact electric utilities and other market participants. For example, California now requires solar power on all new homes after 2019, and New York has effectively blocked utilities from owning distributed generation. The federal government is weighing in as well with new rules to open the wholesale power market for battery storage.

Along with expensive grid upgrades and uncertain regulatory climates ahead, utilities must grapple with the fact that market definition at a regional and local operating level is still nascent making it difficult for utilities to ground their strategies and investment plans in fact-based assumptions. Absent this clarity of direction, utilities need to develop a flexible market model and align their capital allocation strategies to support data-driven predicted outcomes. They’ll need to figure out:

- What is the role of the grid operations considering the emerging, distributed energy markets?

- What new market processes, operating models and business requirements will result from this role?

- What new types of companies will become players in the power grid market of the future?

In answering these types of questions, companies can begin to finetune their capital allocation decisions. And, they’ll start reinventing themselves. For instance, Hong Kong-based CLP (formerly China Light and Power) is exploring a variety of markets outside their regulated territory, including smart cities, DER, microgrids and data centers.

Figure 4. What are your biggest challenges in implementing smart distribution systems? (Select all that apply).

Source: Black & Veatch

Partnering with customers is another strategy that utilities can and likely will follow. Load control programs, for instance, provide non-wires alternatives that enhance reliability without incurring as much cost as system upgrades. Example: ConEdison’s Brooklyn-Queens Demand Management program deferred a $1 billion substation upgrade with a $200 million investment.

Microgrids are another option. Utilities could build microgrids onsite at customer premises that can be used for capacity, backup generation or demand response. Arizona Public Service (APS) is currently cost-sharing on a microgrid owned by Aligned Data Centers. In addition to power back-up for a data center, the microgrid also provides frequency regulation and capacity services to the grid. APS secured regulatory approval to recover costs for the percentage of microgrid capacity that supplies those services.

Looking Ahead

If utilities can prove that they are willing to serve customers in new, creative ways, negotiating with and presenting a business case to regulators will be much easier. Enabling such unique offerings as performance-based rates, community solar and solar-plus-storage for all customer sizes can assist in shifting the utility model enough to slow down the proverbial downward spiral in earnings. Building a marketplace for distributed energy will be a critical step.

Utilities will need buy-in and support from regulators to make changes that align with growing clean-energy mandates and the business transformations they will require. If power providers don’t secure this regulatory vote-of-confidence, they may drive away their bread-and-butter C&I accounts, especially those that are big enough and financially sound enough implement their own renewables, distributed generation or storage solutions. Such defections would make the system more expensive for all remaining customers because utilities would need to invest in new technology to maintain an increasingly complex network and then spread fixed costs among fewer customers.

Try beefing up cyber security, replacing aging infrastructure or investing in new reliability solutions with declining revenues and a customer exodus on your hands. The financial future of utilities is uncertain, and until we get this figured out, today’s power system stands at risk.

Jeremy Klingel is a senior managing director for Black & Veatch management consulting, where he is responsible for developing and delivering the market strategy regarding end-to-end grid-related initiatives for electric utilities. Klingel has led more than two dozen smart grid development projects.

Jeremy Klingel is a senior managing director for Black & Veatch management consulting, where he is responsible for developing and delivering the market strategy regarding end-to-end grid-related initiatives for electric utilities. Klingel has led more than two dozen smart grid development projects.