For most equipment vendors and service providers to the utility industry, 2009 was a year to forget, or at least to look beyond. As a result of an overall slowdown in the economy, credit worries and the short-term “de-stimulating” effect of the American Recovery and Reinvestment Act (“ARRA”) of 2009, utility customers pulled in their horns and postponed or slowed plans for deployments of advanced technology. This meant that equipment vendors and service providers spent less time deploying technology and more time building relationships and supporting the stimulus proposals of their customers. For many smaller industry participants that anticipated a ramp in sales from the roll out of “Smart Grid” technologies, it also meant revisiting their capitalization plans and recalibrating investors’ growth expectations.

Glenn Tofil

Managing Director

England & Company

As expected, the confluence of economic events at the end of 2008 and through much of 2009 had an impact on the activity of investors focused on utility and related “cleantech” investments. According to a report recently released by the Cleantech Group, venture investment in cleantech companies dropped by 33% in 2009 to $5.6 billion compared to $8.5 billion of funding in 2008. While the decline is significant, 2008 was clearly a banner year and represented a peak in optimism related to cleantech initiatives across a number of technologies and market verticals. Based on a reported $1.9 billion of funding in the first quarter of 2010, a high level of optimism seems to be returning.

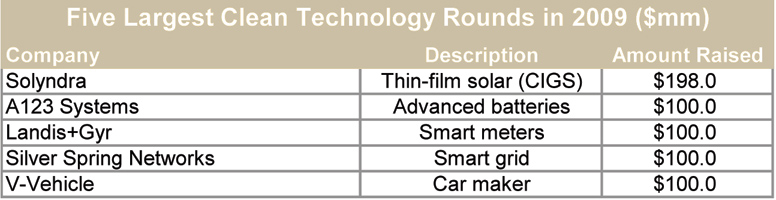

As shown below, there were a number of “megaplays”, which dominated the fundraising landscape in 2009. These included financings by companies involved in large scale solar, energy storage, advanced metering and electric vehicles.

Source: Cleantech Group (cleantech.com)

Source: Cleantech Group (cleantech.com)

Of the $5.6 billion of total cleantech investments made in 2009, the Cleantech Group reported that approximately $1.5 billion in funding went to companies involved in Smart Grid ($414 million) and energy efficiency ($1.1 billion) markets. While the investment in these markets was significant, Project Better Place’s $350 million financing announced in January 2010, demonstrates that on a relative basis, areas such as energy storage and electric vehicle technology appear to be the favorites of investors in the near term.

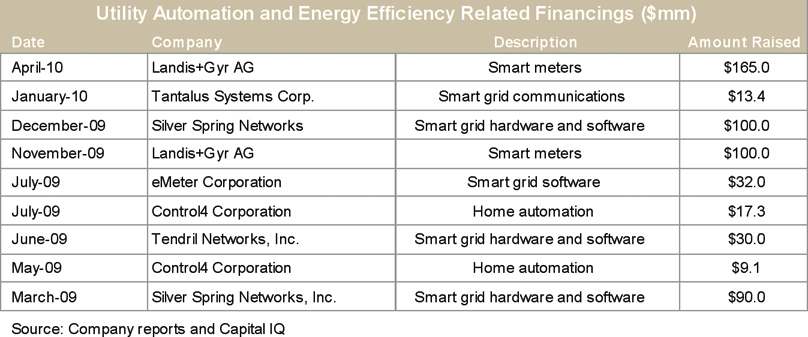

Within utility automation and energy efficiency markets, venture and growth equity investors continued to back seasoned issuers in areas such as home automation/consumer energy management, smart metering and related utility automation technologies. During 2009 and the first quarter of 2010, successful fundraisers included Control4, eMeter, iControl, Landis + Gyr, Silver Spring, Tantalus and Tendril.

While these companies represent a broad cross-section of the market in terms of product or service focus and stage of development and revenue profile, their success in fundraising appears to support the notion that investors prefer companies with significant market opportunity, mass deployable technology and companies with the continuing support of other well-known and highly respected investors.

Despite the success of these companies and relative newcomers on the fundraising scene such as Grid Net and 4Home, a number of well- and lesser-known companies in the utility automation and energy efficiency space remain on the fundraising trail. These include companies in consumer related energy management (hardware and software), advanced metering and demand response, and renewables integration and energy storage technologies. Looking at the number of financial investors with a mandate in these markets and the amount of capital available to them, it is safe to say that there is significant pent up demand for quality investment opportunities. However, despite the pent up demand and increased activity on the part of strategic investors, capital providers remain extremely selective toward financing earlier stage companies and equally as particular in jumping into growth equity investments for more established companies.

During our conversations with investors, concerns regularly expressed include: 1) the potential for rapid change in the competitive landscape or the market structure (i.e. the emergence of a disruptive technology), 2) the pace at which utilities are, or are not, embracing new technologies and whether or not issuers are taking that into account in their capitalization and growth plans, and 3) valuation expectations on the part of issuers.

Differing views on valuation certainly ranks as one of, if not, the most important factors in explaining why more financing transactions are not getting done despite the apparent availability of capital and investment opportunities.

Of the $5.6 billion of total cleantech investments made in 2009, the Cleantech Group reported that approximately $1.5 billion in funding went to companies involved in Smart Grid ($414 million) and energy efficiency ($1.1 billion) markets. While the investment in these markets was significant, Project Better Place’s $350 million financing announced in January 2010, demonstrates that on a relative basis, areas such as energy storage and electric vehicle technology appear to be the favorites of investors in the near term.

Within utility automation and energy efficiency markets, venture and growth equity investors continued to back seasoned issuers in areas such as home automation/consumer energy management, smart metering and related utility automation technologies. During 2009 and the first quarter of 2010, successful fundraisers included Control4, eMeter, iControl, Landis + Gyr, Silver Spring, Tantalus and Tendril.

While these companies represent a broad cross-section of the market in terms of product or service focus and stage of development and revenue profile, their success in fundraising appears to support the notion that investors prefer companies with significant market opportunity, mass deployable technology and companies with the continuing support of other well-known and highly respected investors.

Despite the success of these companies and relative newcomers on the fundraising scene such as Grid Net and 4Home, a number of well- and lesser-known companies in the utility automation and energy efficiency space remain on the fundraising trail. These include companies in consumer related energy management (hardware and software), advanced metering and demand response, and renewables integration and energy storage technologies. Looking at the number of financial investors with a mandate in these markets and the amount of capital available to them, it is safe to say that there is significant pent up demand for quality investment opportunities. However, despite the pent up demand and increased activity on the part of strategic investors, capital providers remain extremely selective toward financing earlier stage companies and equally as particular in jumping into growth equity investments for more established companies.

During our conversations with investors, concerns regularly expressed include: 1) the potential for rapid change in the competitive landscape or the market structure (i.e. the emergence of a disruptive technology), 2) the pace at which utilities are, or are not, embracing new technologies and whether or not issuers are taking that into account in their capitalization and growth plans, and 3) valuation expectations on the part of issuers.

Differing views on valuation certainly ranks as one of, if not, the most important factors in explaining why more financing transactions are not getting done despite the apparent availability of capital and investment opportunities.

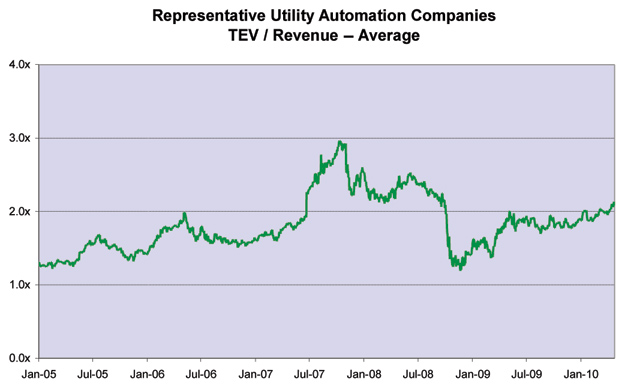

The decline in public equity markets during the second half of 2008 and for most of 2009 has no doubt allowed new investors to challenge the valuation expectations of management teams and existing investors that were set during much better times in the public markets. Public valuations for companies in utility automation and energy efficiency markets peaked during the second half of 2007, which coincided with high levels of M & A activity and strong valuations.

Index includes ABB, Badger, Cooper, ESCO, Itron and RuggedCom, Source: Capital IQ

The rebound in benchmark valuations and an increase in M & A activity should improve the outlook for issuers in the space. Notwithstanding some of the short-term challenges facing issuers in this market, there is definitely reason to remain bullish regarding their long-term success and ability to secure capital to continue their company building efforts and the growth of the market overall. As previously stated strategic investors are quickly becoming significant players in the space. In addition to the well-established venture arms of electrical and utility products companies such as Siemens and Schneider Electric, leading technology companies such as Cisco, Intel and Google have jumped in with significant commitments of capital in support of utility automation and energy efficiency companies.

Corporations like ESCO Technologies (parent of Aclara) are making direct investments in technology partners like Firetide. Going forward, we believe that strategic investors will take an even more active role in the market. This increased level of strategic investor activity coupled with the large amount of capital that remains in the hands of financial investors bodes well for issuers as we emerge from the economic and capital markets malaise of 2009. We expect there to be further momentum as utilities become more aggressive in using ARRA dollars and their own balance sheets to pursue deployments of advanced technologies.

About the Author

Glenn Tofil is a Managing Director with England & Company, an investment bank located in Washington, DC. England & Company is one of the leading merger and acquisition advisors to companies and investor groups in energy efficiency and utility automation markets. More information is available at www.englandco.com.